People purchase a home insurance policy to protect their homes and property against unforeseen circumstances. This type of coverage is not mandatory, but it can be helpful if you ever have a fire, theft, or another disaster that causes damage to your home.

However, there are certain things homeowners should keep in mind when purchasing this type of insurance. Be aware that most home insurance policies only provide coverage for the dwelling itself and not for any personal belongings inside the home. If you have an expensive piece of jewelry or artwork inside your home, your policy may not cover it. To get coverage for these items, you will need to purchase a personal property endorsement, which can add to the cost of your policy.

This blog post will provide an overview of personal liability in home insurance and how it can help protect you and your family.

What Is Personal Liability?

Personal liability insurance is a type of coverage that protects against lawsuits that may arise if you are found liable for damages or injuries on your property. This type of insurance can help protect you from costly legal expenses and any judgments that may be awarded against you.

Personal liability insurance is designed to protect you and your family financially. Your home’s policy’s liability coverage pays for claims of physical injury and property damage caused by people for which you or other covered members of your household are legally accountable.

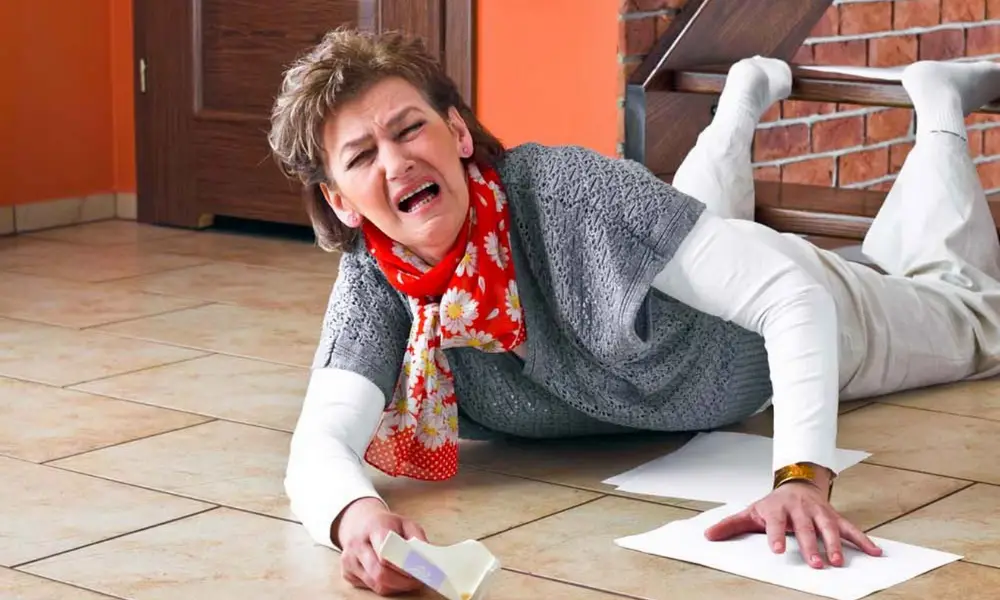

For example, if someone falls down your stairs or your child knocks a ball through a neighbor’s window, damaging an expensive vase, you could be held legally liable.

Many homeowner’s insurance policies include a minimum of $100,000 in personal liability coverage, which means the insurance company can pay up to $100,000 to affected people in a single incident. Higher limitations are available if you believe you require more excellent protection.

Does Home Insurance Cover Personal Liability?

Home insurance policies typically cover personal liability. If you are sued for damages after causing an accident or injury, your home insurance policy will help pay for your legal fees and any settlements you may be required to pay.

Personal liability coverage is crucial because it can help protect your assets if held liable for an accident or injury. Without this coverage, you could be required to pay damages out of your pocket, putting a strain on your finances.

What Is Covered by Homeowners Liability Insurance?

A homeowners insurance policy usually includes personal liability coverage. While no one expects to be held accountable in the event of an accident at their house, liability insurance can assist you to avoid paying out of pocket if the unthinkable happens.

Consider what might happen if someone were to have an unintentional spill down your stairwell. If you are found to be legally accountable for the accident, you may be held liable for your medical expenditures.

Following are the most common types of claims that homeowners liability insurance covers:

Visitors’ Medical Bills

Liability insurance can assist pay for medical expenditures incurred as a result of a visitor’s accidental harm at your house, saving you money on out-of-pocket expenses. Even if that person has health insurance, you could be held liable for the costs if it’s proved that the damage was caused by your negligence — for example, if you failed to repair a broken porch step.

Property Damage

If someone trips and falls on your property because of an obstruction that you didn’t remove, or if a ball gets kicked into a neighbor’s window, homeowners liability insurance can help pay for damages. Your policy may also cover costs associated with repairing or replacing property damaged due to someone being on your property.

Legal Fees

If you’re ever sued for damages after someone is injured on your property, homeowners liability insurance can help pay for your legal fees. This coverage can also assist in paying for a lawyer if you need to defend yourself in court.

Settlements

If you must pay a settlement due to an accident or injury that occurred on your property, homeowners liability insurance can help cover the costs.

Death Benefits

Nobody wants to consider the potential of a deadly accident occurring in their own home, yet it’s impossible to rule out. The ordinary home liability insurance may also cover death benefits for the family of someone who dies in your home or on your property due to an accident.

What Is not Covered by Homeowners Liability Insurance?

While homeowners liability insurance does cover many common types of accidents and injuries, it doesn’t provide coverage for every possible situation.

Some things that are typically not covered by a homeowners liability policy include:

Injuries that Occur Outside of Your Home

If someone is injured while visiting you at a rental property, their medical bills would not be covered by your homeowner’s insurance policy.

Intentional Acts

If you intentionally injure someone or damage their property, your homeowner’s insurance policy will not provide coverage.

Business-Related Activities

If you operate a business out of your home, your homeowner’s policy will not cover any injuries or damages resulting from your work.

Auto Accidents

If someone is injured in an accident on your property, their medical bills would not be covered by your homeowner’s insurance policy.

Natural Disasters

If your home is damaged due to a natural disaster like a tornado or hurricane, your homeowner’s insurance policy will not provide coverage.

How much Does Personal Liability Insurance Cost?

The cost of personal liability insurance varies depending on several factors, including the size of your home, the amount of coverage you select, and your location. Typically, homeowners liability insurance costs between $100 and $300 per year.

How much Personal Liability Insurance Do I Need?

Your liability insurance should be as much as the entire worth of everything you own. Why? Because if you don’t have enough personal liability insurance, a plaintiff can go for your assets.

Let’s look at an illustration.

You have a net worth of $500,000, personal liability insurance of $250,000, and you’re being sued for $400,000 in damages. The plaintiff can go after your assets to cover the remaining $150,000 in damages because your insurance company only covers $200,000 in damages.

What Is the Definition of a Personal Umbrella Policy?

A personal umbrella policy, often known as umbrella insurance, is a type of liability insurance that you can add to your house insurance policy. Your umbrella policy kicks in to cover the remaining costs if your homeowner’s insurance’s liability coverage is exhausted during a claim.

Personal umbrella insurance is often sold in $1 million increments, with some providers offering a maximum coverage of $5 million or even $10 million.

Umbrella plans typically cost roughly $300 per year for the basic minimum coverage. Personal umbrella coverage may be worthwhile if you have more than half a million dollars in combined assets.

Conclusion

Home insurance is a type of property insurance that covers losses to the homeowner’s property. In addition, it also provides personal liability coverage for any accidents or injuries that occur on the property. Suppose someone is injured while on your property; your home insurance policy will help cover the costs associated with their injury. However, it’s important to note that not all home insurance policies provide personal liability coverage. So be sure to check with your insurance company to see if your policy includes this type of coverage.

Leave a Reply